Even the most expert and talented trader can be misled by human irrationality

It is a widespread belief that greed for money has always been driving financial markets since their foundation. Both the fruitful transformations and the toughest crises, which have affected the financial industry, have been strongly guided by the desire of achieving new profits. Undoubtedly, greed is the main reason why investors take excessively risky positions without properly considering the characteristics of their portfolios. The Dot-com bubble and the subprime crisis are the most recent cases of this risk underestimation, but the history of finance provides many similar examples.

In addition to the desire of obtaining easy and quick gains, human behaviour can be influenced by other biases which make traditional rational investors theories inappropriate. Irrational investment decisions, although taken by one trader, can have disastrous consequences for the entire financial institution. The story of Nick Leeson, considered to be the main cause of Baring Bank’s bankruptcy, shows how a solid and centenary institution can lose its fortune due to an employee.

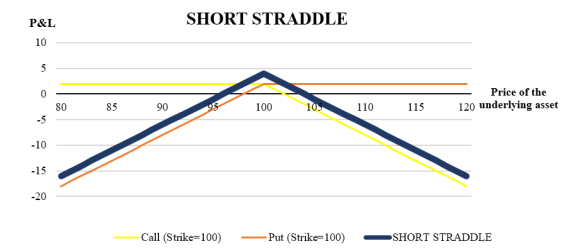

80s and 90s are often considered as the golden age for finance. As new financial markets were opening around the world, in particular in South-East Asia, European and North-American banks were trying to enlarge their business and their activities. Among the several English institutions, Baring, the world’s second oldest merchant bank, was one of the most active in the Singapore exchange, which was considered the most important Asian market. Nick Leeson joined the institution in 1989, after some years spent at Morgan Stanley. As reported in his autobiography, Rogue Trader, after having obtained profits of £ 10 million in 1992, he became “the rising star” at the firm. The success and the ability of the English trader led him to obtain at the age of 28 the full responsibility of the derivatives desk on Singapore International Monetary Exchange. His activity was to consist of only looking for arbitrage opportunities from contracts on Nikkei 225 traded in different exchanges. However, Leeson, seeking larger profits, started to take positions in the market. To hide the losses suffered by his desk, he created a secret account which was registered as client’s account. Between 1992 and 1993 the accumulated losses were negligible. However, at the end of 1994 the account was negative for £ 208 million. The situation became extremely dangerous when Leeson placed a short straddle on Nikkei 225. A short straddle is a strategy consisting in the simultaneous sale of a call and a put option on the same underlying asset with a strike price equal to the price of the underlying. This options-based strategy is profitable for the trader when the price of the underlying asset, the Japanese equity index in this case, does not move too much from the strike price.

However, due to the Kobe earthquake, the index dramatically fell and the succeeding trades placed by the Baring’s trader were completely ineffective. After having left a note reading “I’m Sorry”, he fled Singapore. Nevertheless, Leeson was arrested and spent four years in a Singapore jail.

The Rogue Trader’s case is quite interesting from different points of view. In addition to the importance of risk management in financial institutions, we can highlight how traders’ decisions can be affected by excessive optimism. This bias, as underlined by Kahneman, the father of Behavioural Finance, can assume several forms. In this case, Leeson seems to be affected by the so-called overconfidence bias. Indeed, past positive results made him confident and risk loving. Some colleagues defined him as a “high-flyer who liked to dabble in dare-devil trades”. Furthermore, if we analyse the contracts he tried to trade, we can point out another significant bias. After having suffered the first

dramatic loss, Leeson began placing similar orders waiting for a recovery of Nikkei 225, which did not occur in the short term. From a behavioural point of view, this is called over-reaction to chance events. It is quite common for those gamblers who consider more likely a head after many tails. Also traders believe in the existence of given trend, which, may never actually show up.

Effective risk management along with double-checking of accounts can prevent single traders from taking unbalanced positions. Nevertheless, human behaviour is likely to be negatively affected by a wrong perspective of the reality.