In the stock market, belief formation is one of the most critical challenges. In our “Finance Tuesdays” series, the first three articles are also focused on belief formation: “availability bias and investments” analyses how people estimate probability based on prevalence or familiarity, “Book review ‘a crisis of beliefs’” is about a novel interpretation of the credit cycle based on representativeness and diagnostic expectations, “Dividend anomaly” introduces mental accounting and its deviation of classical corporate finance theory. The post of today could be seen as an extension to the previous book review on “A crisis of beliefs”. The theme is extrapolation. Yes, the word may sound strange and if you google it you would definitely be lost, but after reading this article you will find this idea surprisingly simple and intuitive. Simply put, if you see a recent week of high returns and therefore expect tomorrow’s returns to be high, you are probably an extrapolator.

How would you make an investment in the stock market? As Prof. Aswath Damodaran at New York University pointed out in one of his classes, you move when you find a mistake in the current valuation and hope that the market will correct itself. How could you detect a mistake in current valuation? You would need to compare the “correct” valuation with the market price. To get a correct valuation, you need to predict the future cash flow and impute it in a DCF model. If you are not a big fan of intrinsic valuation, you need to at least predict how the price (returns) will be in the future to find out trading opportunities. If you are a derivative trader, you may also need to predict the volatility in the future!

But, how to predict the future? There are a lot of ways and underlying logical arguments, but one of the most common and intuitive ways of predicting is extrapolation. Formally speaking, an extrapolator is an individual whose estimate of the future value of a quantity is a positive function of the recent past values of that quantity (Barberis, 2018). Why is this so important and useful for behavioural finance? Because it could help understand a lot of puzzles deviating classical theories in the stock market. One of the puzzles is that of medium-term momentum but long-term reversal. A simple explanation of the two models is the following:

A stock’s return over the past six months or one year predicts the stock’s subsequent return with a positive sign in the cross-section, while A stock’s return over the past three to five years predicts the stock’s subsequent return with a negative sign in the cross-section (Barberis, 2018).

The simple model of extrapolation could amazingly account for the phenomenon. First, we should imagine an extrapolator who believes that the more recent news is the most important. Therefore, his expected future price change is a weighted average of the past price changes that puts more weights on the more recent changes (Barberis, 2018). Now we are all set.

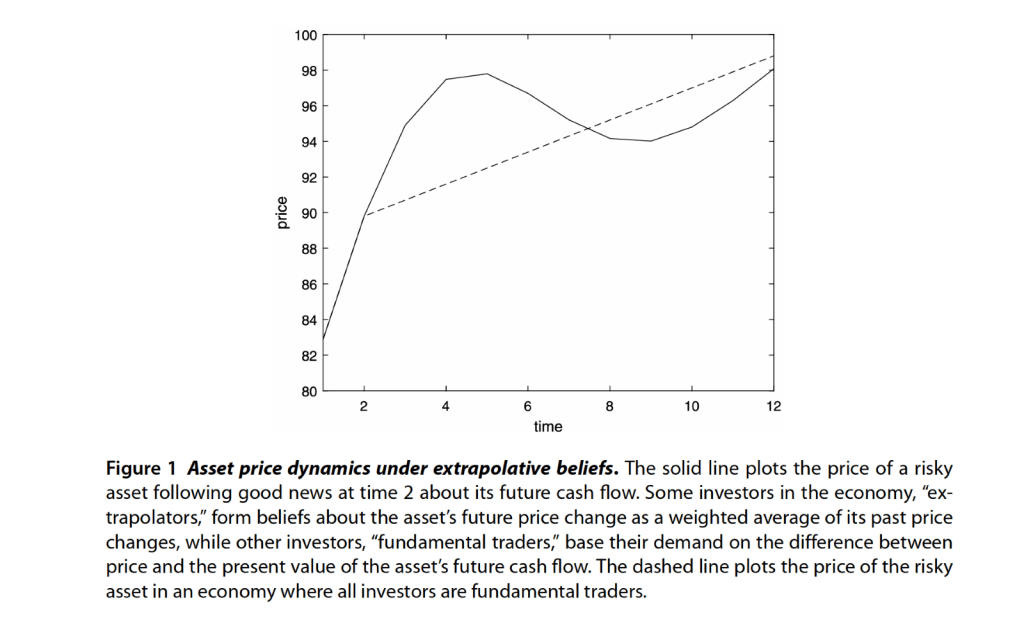

From Barberis’s article: Psychology-Based Models of Asset Prices and Trading Volume.

As we could see from this picture, at date 2 the positive shock pushes the price up. At date 3 the extrapolators, after observing the large price increase, become more optimistic about the future price change and push the price up higher. At date 4 and 5 a similar process follows. At date 6, however, the price falls because the largest past price increases (at date 2 and 3) have been gradually discounted and therefore the extrapolators are less confident. Similar reasoning could go on for the rest. And it could partly explain momentum and reversal in this way: a positive price change at date 2 pushes the price further up at date 3, while a high return in date 1-5 is followed by a poor return over the next few periods. The underlying logic could be that if the asset has had a good long-term past return, this is a sign that extrapolators have been buying it aggressively, causing it to become overpriced; the overvaluation is then followed by low returns (Barberis, 2018).

Why would people be an extrapolator? A lot of discussions have been made on this interesting topic and I would like to focus on heuristics approach. Representativeness heuristics, first proposed by Kahneman and Tversky, shows that when people answer the question “What is the probability that object A belongs to class B?,” or “What is the probability that data A are generated by model B?,” their answers are based on the extent to which A is representative of B; in other words, the extent to which A reflects the essential characteristics of B (Barberis, 2018). More formal and extensive definitions on representativeness could be seen in other works such as Gennaioli’s paper “What comes to mind”. If people are using this heuristic, they may deduct that the asset’s mean return is high when they see several periods of high returns, neglecting the base rate of a high mean return asset. Extensive arguments could also be found in the book “A crisis of beliefs” which our series had reviewed before. Another heuristic in play maybe the “law of small numbers”, or “misconceptions of chance”, also introduced by Tversky and Kahneman. People think, incorrectly, that even a small sample of data will reflect the properties of the model that generated it (Barberis, 2018). Then, the extrapolative thinking could be explained: even if people only observe a short series of high returns, they would believe that it reflects the true mean return.

References

Barberis, N. (2018). Psychology-Based Models of Asset Prices and Trading Volume. In Handbook of Behavioral Economics, Volume 1.